Stock Markets Remain Steady as Investors Await Jackson Hole Meeting: Bloomberg Report

The stock market showed minimal movement on Monday as traders exhibited caution ahead of the Federal Reserve's annual Jackson Hole symposium, where new guidance on interest rates is anticipated. After a strong rally the previous week, major indices like the S&P 500 saw little change, reflecting the market's cautious sentiment. The S&P 500 futures remained almost flat, and Nasdaq 100 futures saw a slight dip of 0.1%.

The tech sector had some notable activity, with shares of Advanced Micro Devices Inc. gaining in premarket trading. The company recently acquired data centre technology, sparking investor interest. In contrast, European defence companies, including Rheinmetall AG, saw their shares decline after a report that Germany might halt new aid requests for Ukraine due to budget concerns.

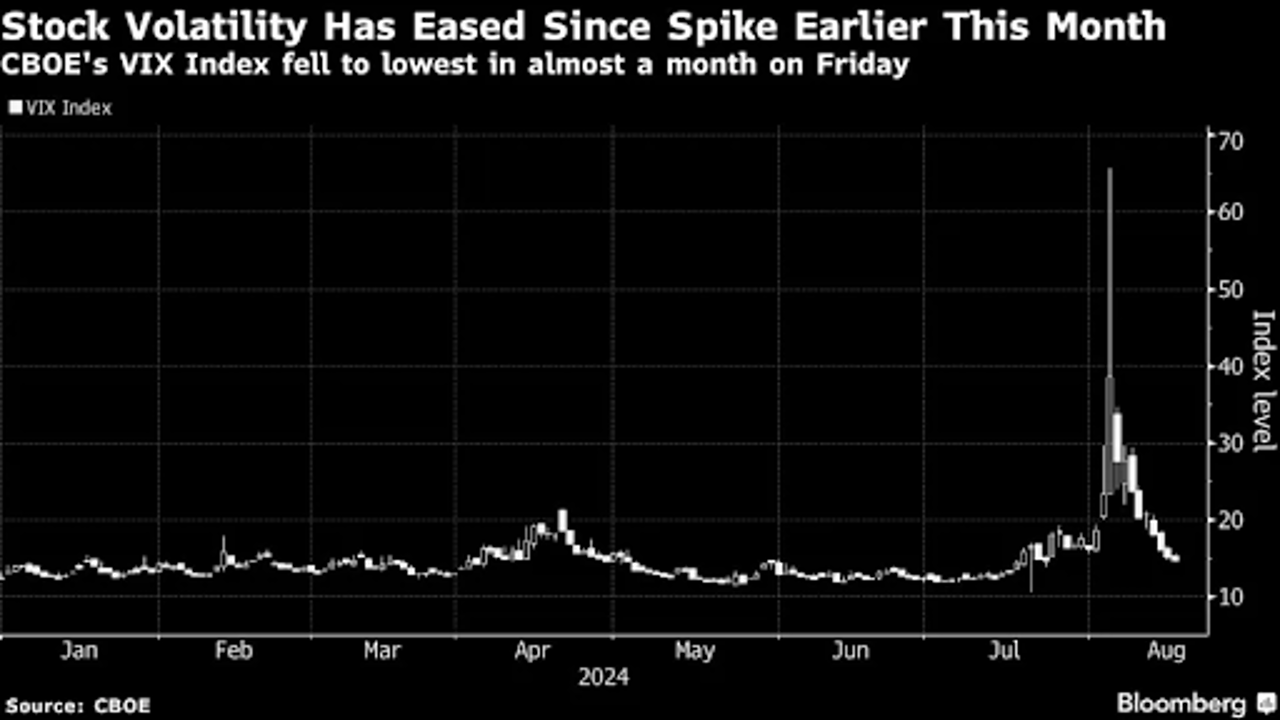

Investors entered the week carefully, following last week's rebound that brought the S&P 500 close to record levels. The market’s recovery has been gradual, with investors re-entering the scene after a sharp dip on August 5th. Louise Dudley, a global equities portfolio manager at Federated Hermes, observed a more measured market tone, noting, "There's a sense of stability now. We're watching for opportunities in large-cap stocks that still present growth potential."

All eyes are on the upcoming Jackson Hole symposium, where Fed Chair Jerome Powell is expected to provide insights into the central bank’s monetary policy strategy. Seth Carpenter, Morgan Stanley’s chief global economist, emphasized that Powell’s address would likely outline the Fed’s medium-term approach.

The anticipation of a "soft landing" for the economy is helping to boost investor confidence. Goldman Sachs recently reduced the probability of a U.S. recession in the next year to 20% from 25%, following strong retail sales and jobless claims data. The firm suggested that if the upcoming August jobs report is favourable, they might lower the recession odds even further to 15%.

Meanwhile, the oil market is under pressure, with prices dropping for the fourth time in five sessions. Traders are monitoring U.S.-led efforts to broker a ceasefire in Gaza, along with rising tensions in the ongoing Russia-Ukraine conflict.

The U.S. dollar weakened as traders began reassessing their bets on a potential return to the White House by Donald Trump. Jane Foley, Rabobank’s head of FX strategy, pointed out that recent polling data and Vice President Kamala Harris’s strong performance have led the market to question earlier assumptions. This shift in sentiment could lead to a softer dollar.

As the week unfolds, several key events are expected to shape the market. The U.S. Democratic National Convention begins on Monday, with Vice President Kamala Harris set to deliver her acceptance speech later in the week. Additionally, the U.S. and South Korea are kicking off their joint military exercises, and significant economic data from China, Canada, and Europe is due for release. Central banks in Sweden, Turkey, Indonesia, and Thailand are also expected to announce interest rate decisions.

The market is poised for a busy week, with the Federal Reserve's Jackson Hole symposium on Friday being the main event. Investors will be closely watching for any indications of future monetary policy from Fed Chair Jerome Powell, alongside comments from Bank of England Governor Andrew Bailey.